Introduction: Your Customers Have Moved On — Have You?

Picture this: a customer walks into your store, finds exactly what they're looking for, heads to the register with a smile on their face — and then discovers you only accept cash. The smile disappears. The product goes back on the shelf. And your competitor down the street (who accepts literally everything except gold doubloons) just got a new customer.

The way people pay has changed dramatically, and it's changed fast. According to the Federal Reserve's 2023 Diary of Consumer Payment Choice, cash now accounts for fewer than 20% of all transactions in the United States. Meanwhile, digital wallets, contactless payments, and buy-now-pay-later options are surging in popularity. Your customers aren't just hoping you'll keep up — they're expecting it.

The good news? Expanding your payment options isn't as complicated or expensive as it used to be. This guide breaks down the modern payment methods your retail customers expect, explains why each one matters, and helps you figure out which ones make the most sense for your business. No finance degree required.

The Payment Methods You Absolutely Need to Have

Contactless and Mobile Payments

If you don't accept tap-to-pay yet, this is your loudest wake-up call. Contactless payments — including cards with NFC chips and mobile wallets like Apple Pay, Google Pay, and Samsung Pay — have gone from novelty to necessity. The COVID-19 pandemic supercharged adoption, and customers simply never looked back. Nobody wants to dig through their wallet anymore when they can just tap their phone and move on with their lives.

The hardware investment is minimal. Most modern point-of-sale (POS) terminals support contactless payments right out of the box, and if yours doesn't, an upgrade is likely overdue anyway. Beyond the customer experience, contactless payments are faster, which means shorter lines, happier customers, and more transactions in the same amount of time. That's not just convenience — that's revenue.

Credit and Debit Cards (Yes, All of Them)

This might seem obvious, but you'd be surprised how many small retailers still selectively accept cards — only Visa, or only debit, or nothing under a $10 minimum (which, by the way, is a great way to frustrate people buying a $7 item). Accepting all major card networks — Visa, Mastercard, American Express, and Discover — removes friction from the purchase process. And removing friction is the name of the game in retail.

Processing fees are the usual objection here, and that's fair. American Express does carry higher interchange rates than Visa or Mastercard. But consider the math: how many Amex customers have you turned away? How many of them didn't come back? The lost revenue almost always outweighs the extra processing cost. If fees are a real concern, work with your payment processor to negotiate rates — it's more possible than most business owners realize.

Buy Now, Pay Later (BNPL)

Buy Now, Pay Later services like Afterpay, Klarna, Affirm, and Sezzle have exploded in popularity, particularly among younger shoppers. These platforms let customers split their purchase into installments — often interest-free — while you get paid upfront. It's a genuinely brilliant arrangement for everyone involved.

BNPL is especially powerful for higher-ticket items. Customers who might hesitate at a $300 purchase often have no problem with four payments of $75. Studies have shown that retailers offering BNPL see increased average order values and reduced cart abandonment. If your products have any meaningful price point, this is worth serious consideration.

Let Technology Handle the Welcome Mat

Streamline the In-Store and Phone Experience With Smart Tools

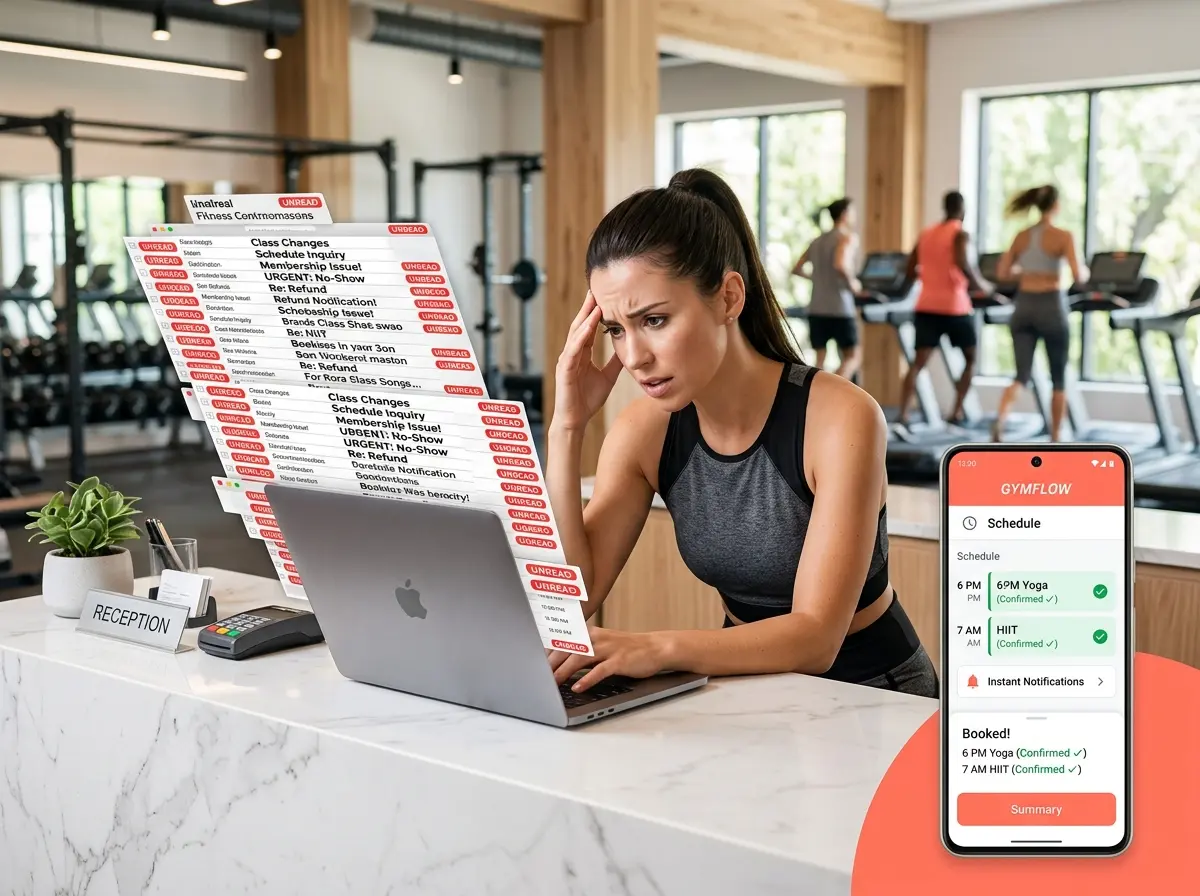

Modernizing your payment options is one piece of the puzzle — but the overall customer experience matters just as much as how they pay. That's where Stella, an AI robot employee and phone receptionist, fits naturally into the picture. In your physical location, Stella stands as a human-sized AI kiosk that greets customers proactively, answers their questions about products, services, hours, and policies, and promotes your current deals — all without pulling your staff away from what they're doing.

Stella also answers your business phone calls 24/7, handling inquiries with the same knowledge she uses in person. Whether a customer is calling to ask about your accepted payment methods, your return policy, or whether you carry a specific product, Stella has it covered. She can forward calls to your team when needed, take voicemails with AI-generated summaries, and send push notifications to managers — so nothing falls through the cracks. At $99/month with no upfront hardware costs, she's the kind of employee who never calls in sick and never asks for a raise.

Emerging and Niche Payment Options Worth Knowing About

Cryptocurrency: Trendy, But Know Your Audience

Accepting Bitcoin or Ethereum makes for a great conversation piece, but let's be honest — it's not going to drive a wave of new foot traffic to your boutique candle shop. Crypto payment adoption in retail remains niche, and the volatility of digital currencies adds a layer of financial complexity that most small business owners don't need. That said, if your target customer base skews tech-forward or you operate in an industry where crypto enthusiasts are a significant segment, it's worth exploring. Payment processors like BitPay and Coinbase Commerce make it relatively straightforward to accept crypto without holding it yourself.

The bottom line: don't feel pressured to accept crypto just because it sounds futuristic. Focus on the payment methods your actual customers want, and revisit this one when the landscape matures.

QR Code Payments and Payment Links

QR code payments deserve more attention than they typically get in the U.S. market. Common in Asia for years, they're gaining ground domestically — especially in restaurants, but increasingly in retail as well. Customers scan a code with their phone camera, confirm the amount, and pay directly from their banking app. It's fast, hygienic, and doesn't require any card hardware at all.

Payment links are a related concept worth embracing, particularly if you do any amount of business outside your physical storefront. Whether you're invoicing a wholesale client, selling at a pop-up market, or following up with a customer who placed a special order, a simple payment link sent via text or email lets them pay instantly from wherever they are. Tools like Square, Stripe, and PayPal all make this dead simple to set up.

Gift Cards and Store Credit Programs

Gift cards often get overlooked in conversations about payment methods, but they're genuinely powerful retail tools. They bring in cash upfront, often before a single product changes hands. They introduce new customers to your store when given as gifts. And statistically, customers tend to spend more than the gift card value when redeeming — a phenomenon retailers have happily observed for decades. Digital gift cards, which can be delivered via email and redeemed in-store or online, are increasingly expected and easy to implement through most modern POS systems.

Quick Reminder About Stella

Stella is an AI robot employee and phone receptionist built for businesses of all sizes — from busy retail stores to solo service providers. She greets customers in person, answers your phones around the clock, promotes your deals, and keeps your staff free to focus on what matters most. At just $99/month with no upfront hardware costs and easy setup, she's one of the most practical investments a modern business owner can make.

Conclusion: Make It Easy to Give You Money

At the end of the day, that's really what this is all about. The more ways you give customers to pay you, the fewer reasons they have to walk away empty-handed. Here's a quick action plan to get started:

- Audit your current POS system. Does it support contactless payments and mobile wallets? If not, contact your provider — an upgrade may be simpler than you think.

- Add a BNPL option. If your average transaction is over $100, this is a high-priority move. Afterpay and Klarna both have straightforward merchant onboarding processes.

- Launch a digital gift card program. Check whether your existing POS or e-commerce platform supports it — many do natively.

- Set up payment links. Even if you're primarily a brick-and-mortar business, having this capability for special orders and remote customers is worth the five minutes it takes to configure.

- Drop the cash minimum. Seriously. Just drop it. The goodwill alone is worth more than the few cents you save on processing fees.

Modern retail is competitive, and customer expectations only move in one direction: upward. The businesses that thrive are the ones that meet customers where they are — including at the payment terminal. Get your payment options in order, pair them with a seamless in-store and phone experience, and you'll be well ahead of the competitors who are still asking if anyone has exact change.